Key Findings

Avant Protocol, with its distinctive senior/junior tranche design and fully on-chain transparent strategy execution, has grown into a hundred-million-dollar yield-bearing stablecoin protocol. Over more than a year of operation, the senior tranche (savUSD) and junior tranche (avUSDx) have delivered cumulative appreciation of 16% and 17.4% respectively — an impressive track record of strategy execution.

But does the yield redistribution created by tranching equate to real risk isolation?

Through comprehensive on-chain portfolio look-through and data tracking of the protocol's underlying assets, we found that Avant's actual risk profile diverges significantly from the theoretical "buffer" model:

- Portfolio look-through: Highly concentrated leveraged carry. Despite positioning itself as a multi-strategy framework, during periods with reliable tracking coverage, over 80% of its underlying exposure has been concentrated in a single type — ~10x leveraged Ethena (USDe/sUSDe) lending rate arbitrage.

- Homogeneous risk: Identical exposure beneath nominal tranching. The senior tranche, junior tranche, and reserve fund appear to form three layers of defense, but all are directly or indirectly exposed to Ethena. When systemic risk strikes, all three layers move in lockstep, lacking substantive risk isolation.

- Stress test replay: The "procyclical" fragility of the buffer. During the real extreme market events of October–November 2025 (a USDe flash crash on exchanges and the Stream Finance liquidation), on-chain transaction records reveal: on the same day USDe price pressure emerged (Oct 10), a single large holder submitted $1.4M in redemption requests within hours; the next day (Oct 11), they fired off 16 requests totaling $8.7M in just 13 minutes. Due to avUSDx's fixed 7-day redemption waiting period, these requests settled on Oct 17, causing the buffer ratio to plunge from 18.4% to 9.8%. The protocol's survival owed more to Aave's oracle pricing mechanism than to the tranche buffer.

Conclusion: Avant is a yield product with excellent leveraged operations capability, but investors need a clear understanding: you are participating in leveraged Ethena lending rate arbitrage, and should not treat the tranche structure as a safety net against extreme downside risk.

I. What Is Avant

Avant Protocol is a yield-bearing stablecoin protocol deployed on Avalanche. Its core feature is a tranche structure — senior and junior layers supplemented by a reserve fund buffer, promising risk protection for senior tranche users.

After depositing USDC to mint avUSD, users can choose:

- Stake as savUSD (senior tranche): Earn stable yield. Launched December 2024, cumulative appreciation ~16% (annualized ~13%), recent annualized ~8%

- Hold avUSDx (junior tranche, aka MAX avUSD): Accept higher volatility for higher returns. Launched July 2025, cumulative appreciation ~17.4% (annualized ~25%), recent annualized ~14.5%

The protocol also maintains a Reserve Fund (currently $1.27M), positioned as the first line of defense when losses occur.

Avant has been running for over a year with total AUM approaching $150M, of which avUSD accounts for nearly $130M. Senior tranche savUSD holds ~$89M (71%), junior tranche avUSDx ~$22M (18%), reserve fund ~$1.27M (1%), with the remaining ~$13M (10%) in the minting contract and freely circulating avUSD.

II. Where the Yield Comes From: An Extreme Leverage Spread Business

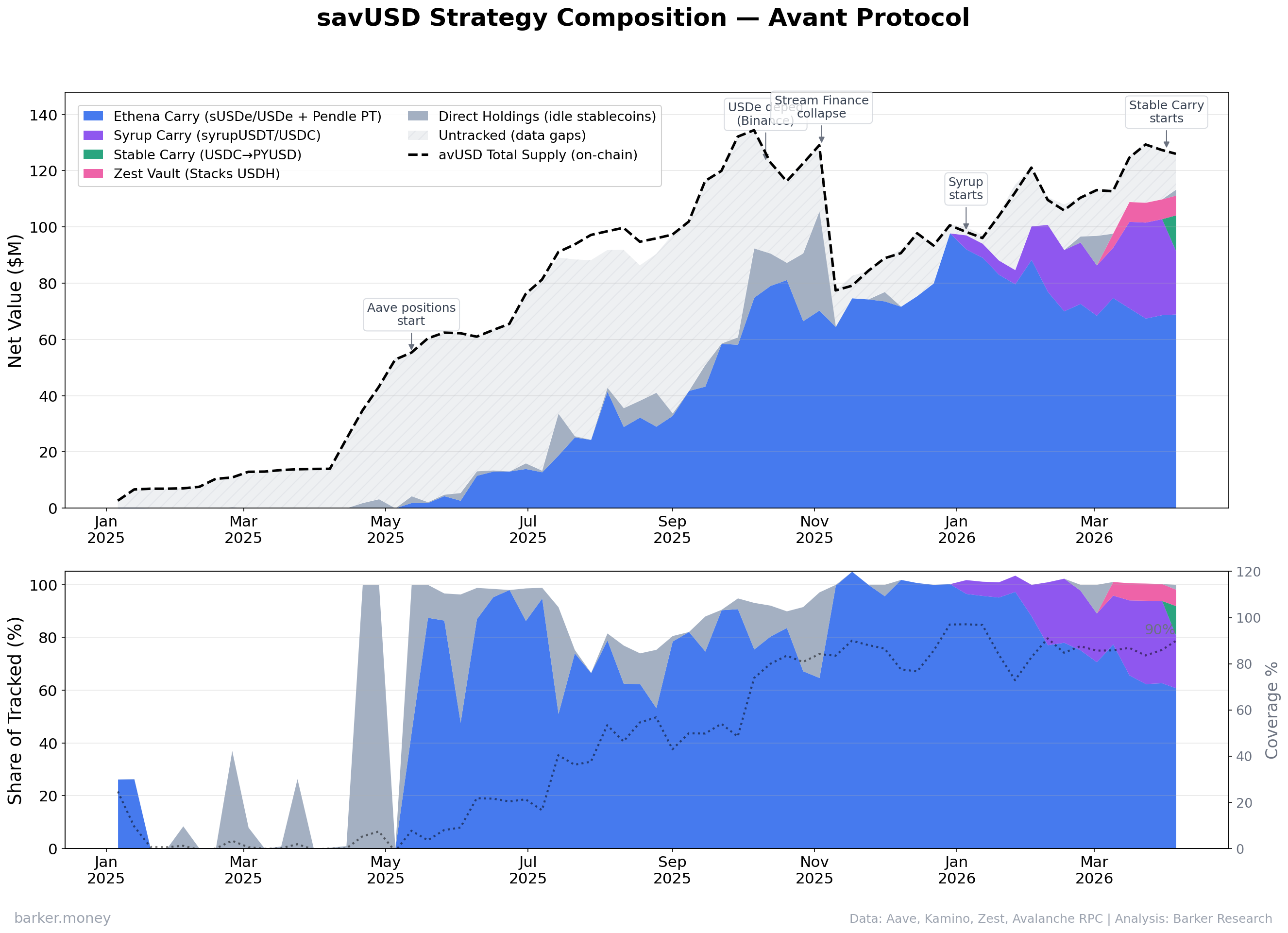

Strategy Breakdown: The Nominal Multi-Framework vs. Highly Concentrated Underlying Business

Avant officially describes its strategy as a "multi-strategy framework," listing five categories: Basis Trades, Lending Rate Arbitrage, Yield Trading, Lending Markets, and Other Strategies.

After tracking on-chain positions, we found that lending rate arbitrage is the de facto sole driver.

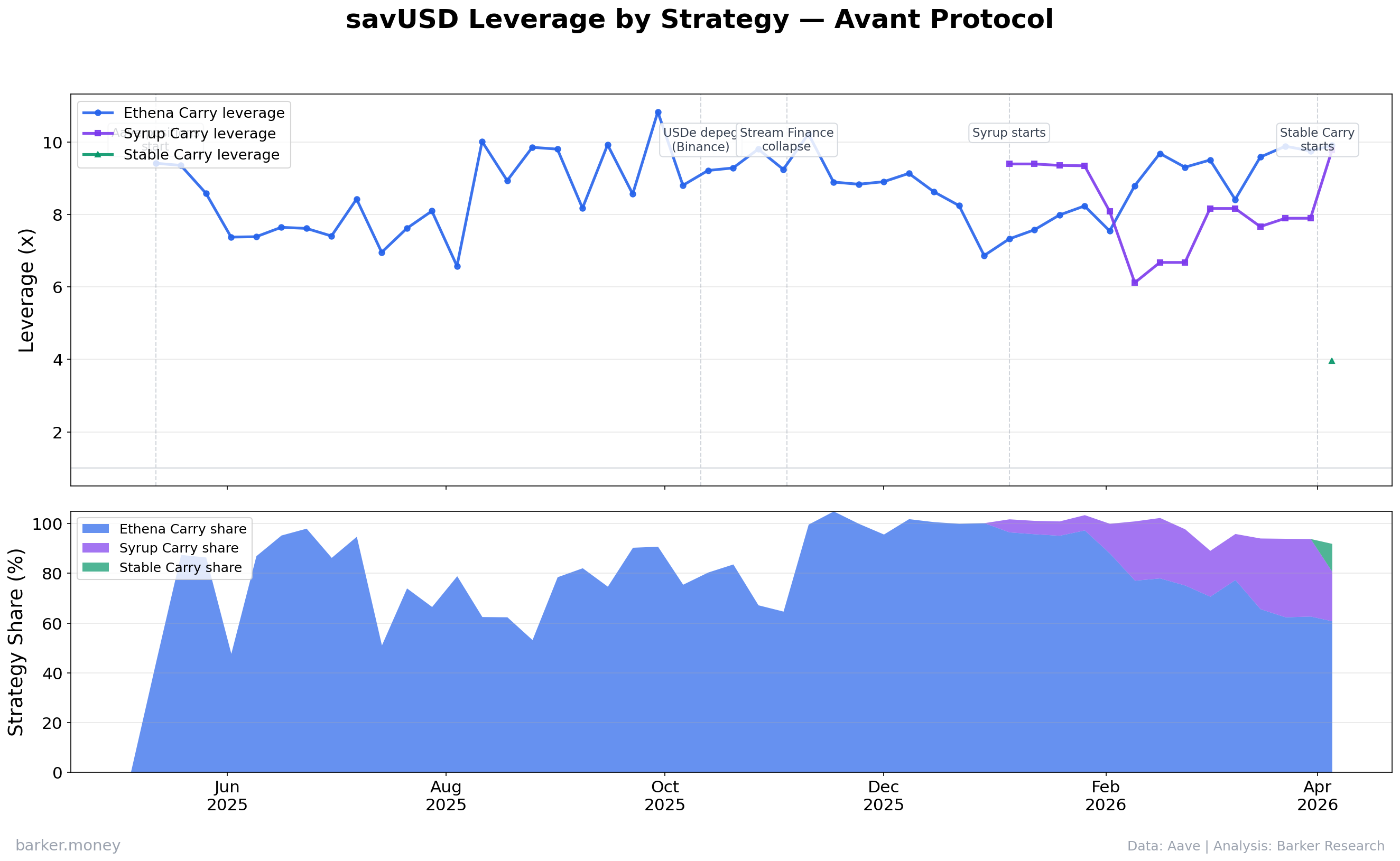

Note: Coverage was low before August 2025 (<30%), so early proportions only reflect the tracked portion and do not represent the full strategy composition. Coverage refers to the share of total AUM explainable by the 23 strategy wallets currently disclosed by the protocol — in earlier periods, the protocol may have used other wallets not included in its latest disclosure, making full historical position reconstruction impossible. From October 2025 onward, coverage has been consistently above 73%, providing reliable data. During this period, Ethena carry (blue) has dominated. From 2026, Syrup carry (purple) gradually joined, bringing Ethena's share down from 90%+ to ~55%, but all strategies are fundamentally the same type: lending rate arbitrage.

How the Strategy Works

The logic is straightforward:

- Deposit high-yield stablecoins (sUSDe, syrupUSDT, etc.) into Aave V3 as collateral

- Borrow USDT/USDC at a lower rate

- Use borrowed funds to purchase more high-yield stablecoins, deposit back into Aave, and repeat

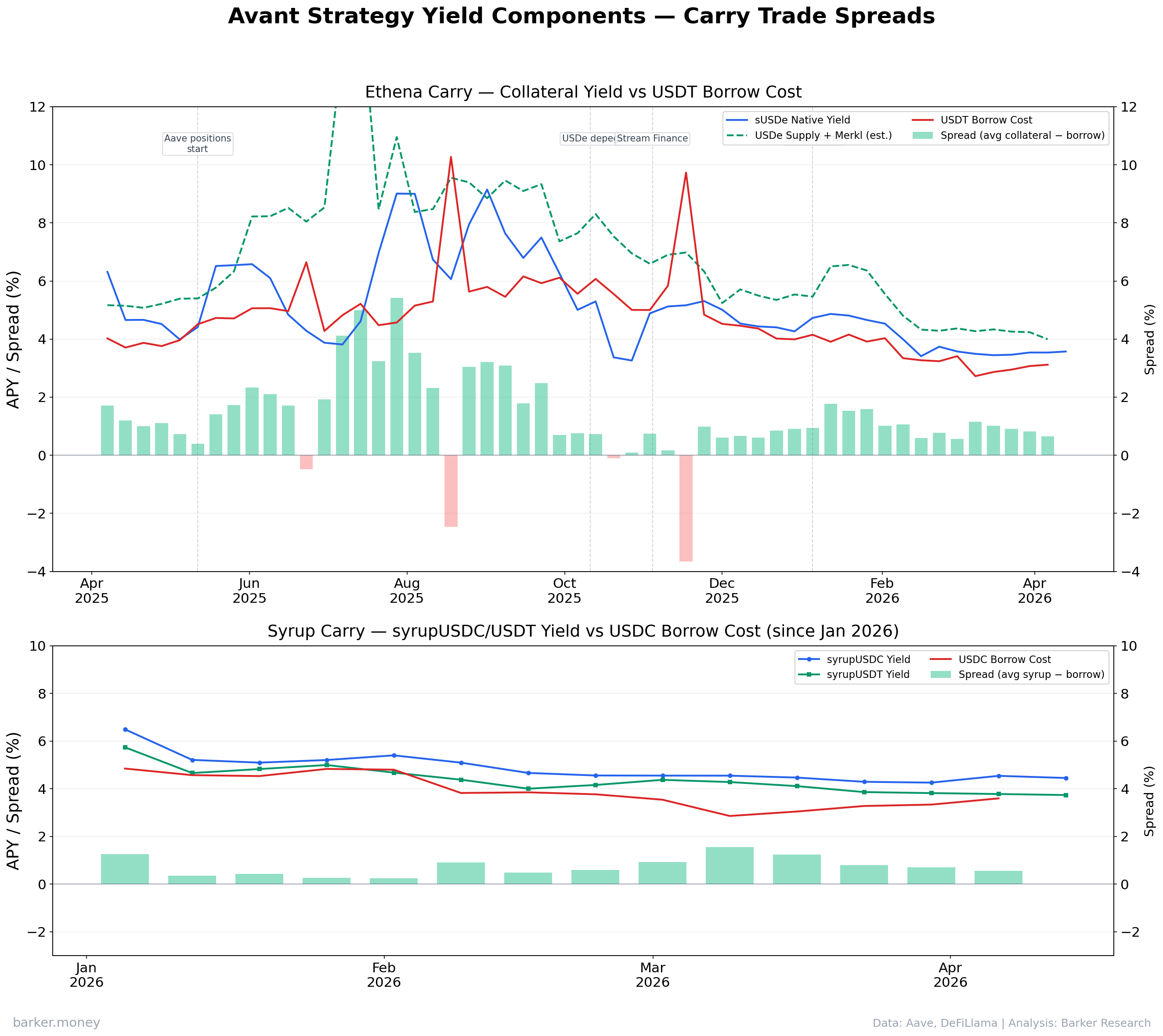

- Earn the spread between "collateral yield − borrowing rate," amplified by leverage

Top: Ethena carry spread — sUSDe yield vs USDT borrowing cost. Mid-2025 spread was 4–6%, since compressed to 1–2%. Bottom: Syrup carry spread (from 2026).

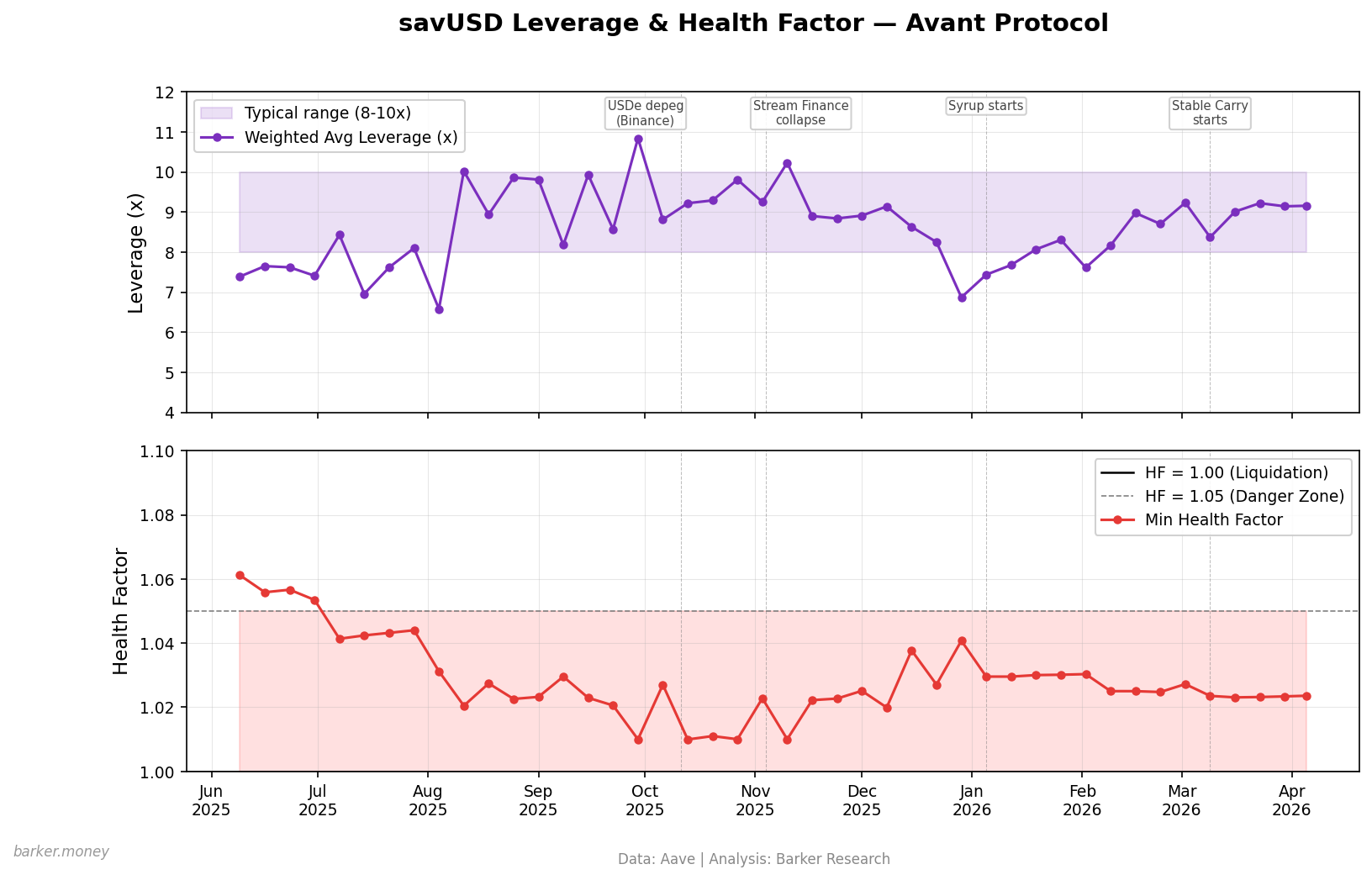

How Leverage Amplifies Returns

As of late March 2026, senior tranche leverage across chains ranges from 9.6x to 10.2x. The leverage math:

10x leverage means $1 of equity controls $10 of collateral and $9 of borrowing. If collateral yields 5% and borrowing costs 3%:

Gross strategy return = 10 × 5% − 9 × 3% = 23%

This explains why a seemingly modest 1–2% spread can produce double-digit strategy returns. But leverage also amplifies risk on the downside — at 10x leverage, a mere low single-digit percentage (~1–2%) decline in collateral value could breach the Liquidation Threshold, triggering on-chain liquidation.

Looking at the spread chart, mid-2025 sUSDe yield was ~6–8%, USDT borrowing rate ~2–3%, spread 4–6%. At 10x leverage, gross strategy returns reached 30–50% — this is why early savUSD APY hit 20–25%.

But spreads have since compressed: current sUSDe yield is ~4–5%, borrowing rate ~3%, spread just 1–2%. At the same 10x leverage, gross strategy return drops to ~10%. After fees, savUSD holders currently receive ~8%.

Top: Weighted average leverage ratio (long-term 8–10x), with key events annotated. Bottom: Weekly minimum Health Factor, persistently in the 1.02–1.05 danger zone, never far from the liquidation line.

How Concentrated Is It

Ethena: Ethena-related assets (including sUSDe, USDe, and Pendle PT-USDe derivatives) have consistently comprised 55–95% of tracked collateral. During the November 2025 crisis, this reached 94%. As Ethena spreads declined, Avant began diversifying into more carry trade varieties — adding Syrup carry (syrupUSDT/syrupUSDC) in early 2026, bringing Ethena's share down to ~55%. But strategy types remain homogeneous lending rate arbitrage, falling short of the officially advertised multi-strategy landscape.

Aave: Before Kamino (Solana) launched in January 2026, Aave V3 accounted for >90%. Currently down to 73%, still highly concentrated.

Gross strategy return is ~10%, but savUSD holders only receive ~8% — where does the difference go?

III. Mechanism Examination: Homogeneous Risk and Liquidity Game Theory Under Extreme Conditions

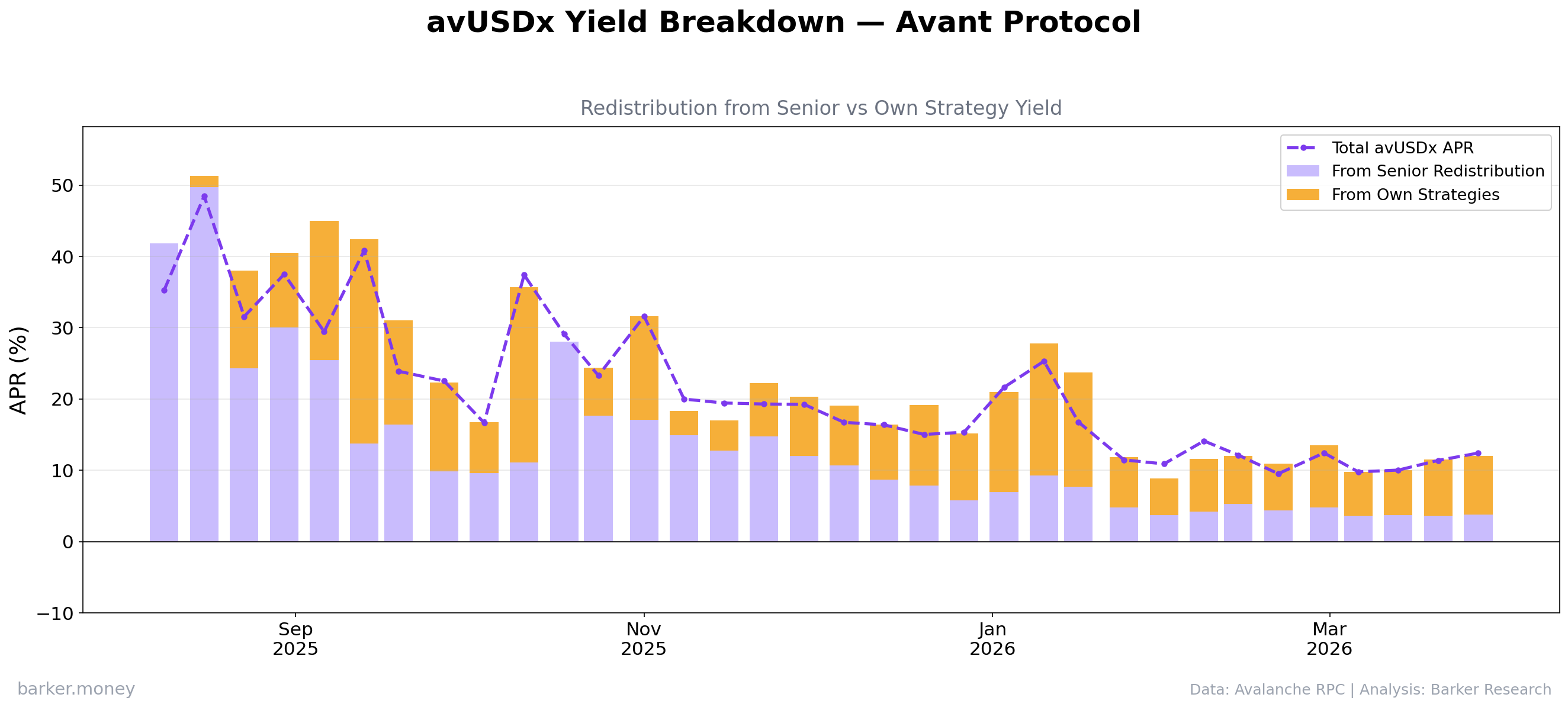

How Yield Is Distributed

Gross yield from senior tranche strategies flows three ways:

| Destination | Share | Mar 2026 Weekly Avg | Notes |

|---|---|---|---|

| savUSD holders | 80% | ~$132K | Protocol periodically injects avUSD into the savUSD contract |

| Junior redistribution | 10% | ~$16K+ (estimated) | Manifests as part of avUSDx weekly price jumps, indistinguishable from proprietary returns |

| Protocol performance fee | 10% + variable | ~$16K+ (estimated) | Protocol + management team |

This theoretically forms the basis for senior tranche users to exchange yield for junior tranche risk protection. For savUSD holders, the effective cost is ~1% annualized yield (from ~9.7% gross to ~8% net). For avUSDx holders, this redistribution contributes ~3.8% additional annualized return — combined with ~8.2% proprietary strategy returns, totaling ~12% APR.

Purple represents redistribution from the senior tranche, orange represents proprietary strategy returns. Early on, redistribution dominated (junior tranche was just starting); over time, proprietary returns became the primary source.

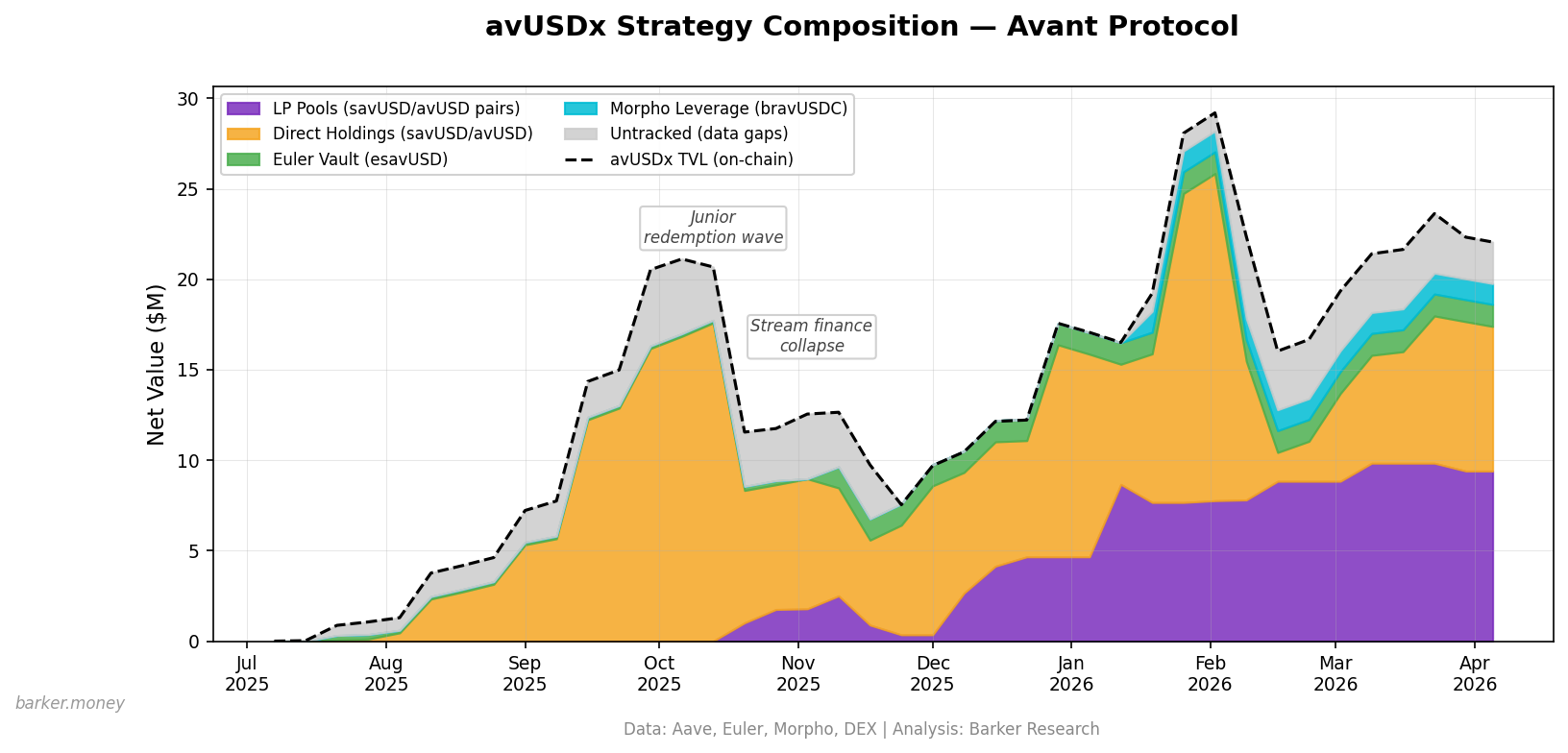

What Does the Junior Tranche Actually Hold

Orange (savUSD/avUSD direct holdings) consistently dominates. Purple represents DEX LP (Pharaoh V3, TraderJoe LB, etc. savUSD/avUSD pools), green represents Euler vault. Dashed line shows avUSDx on-chain TVL.

The junior tranche's 7 strategy wallets primarily hold savUSD/avUSD DEX LP positions and direct holdings. These assets earn LP fees and some incentive yields, while maintaining a portion of direct holdings potentially for redemption readiness.

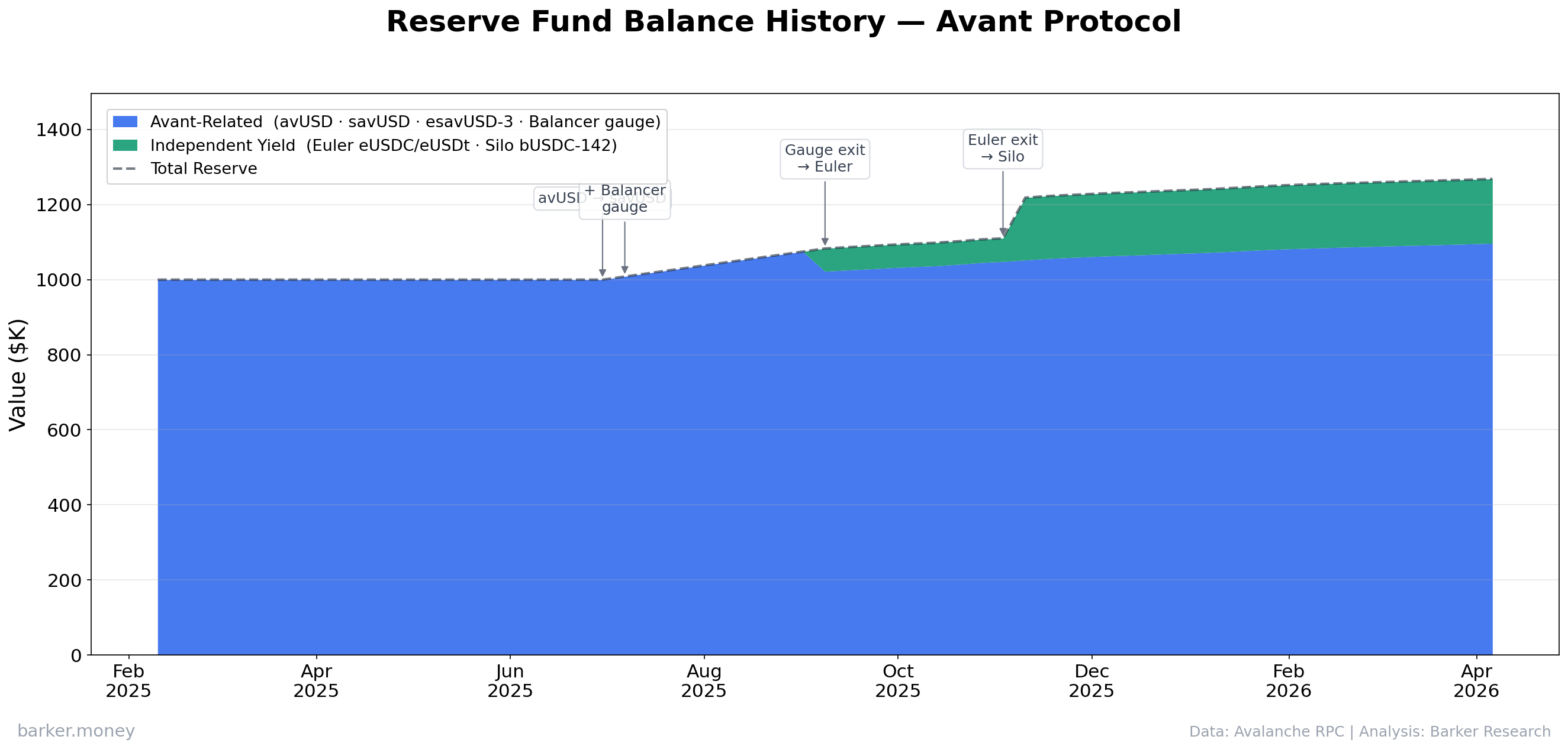

Reserve Fund: $1.27M in savUSD

Blue represents Avant-related assets (primarily savUSD), green represents independent yield-bearing assets (Silo bUSDC, etc.). Total balance has remained essentially flat at $1M–$1.27M over 14 months.

The reserve fund represents just 1.4% of savUSD TVL. On-chain data shows that over 14 months of operation, despite the protocol generating considerable performance fee revenue, no injections were made into the Reserve Fund. The reserve pool's growth came primarily from its own yield, and its scale is a drop in the bucket against extreme risk scenarios. Moreover, the reserve's primary asset is savUSD itself.

All Layers, One Set of Risks

At this point, experienced readers may have already noticed:

- Senior tranche: High-leverage Ethena carry trade, core risk is sUSDe/USDe depegging.

- Junior tranche: Holds savUSD/avUSD LP — the underlying is the senior tranche strategy's own output.

- Reserve fund: Primary asset is still savUSD. This means the protocol is using its own risk asset as collateral. If the underlying suffers extreme losses, the reserve's value shrinks in lockstep — a reflexive downward spiral that cannot serve as a genuine external hedge.

All three layers of protection face the same set of risk exposures. If the Ethena carry trade suffers systemic losses, the senior tranche, junior tranche, and reserve fund would all be impaired simultaneously — there is no genuine risk isolation.

Stress Test Replay: The "Life-or-Death 1%" During the 10/11 Extreme Event

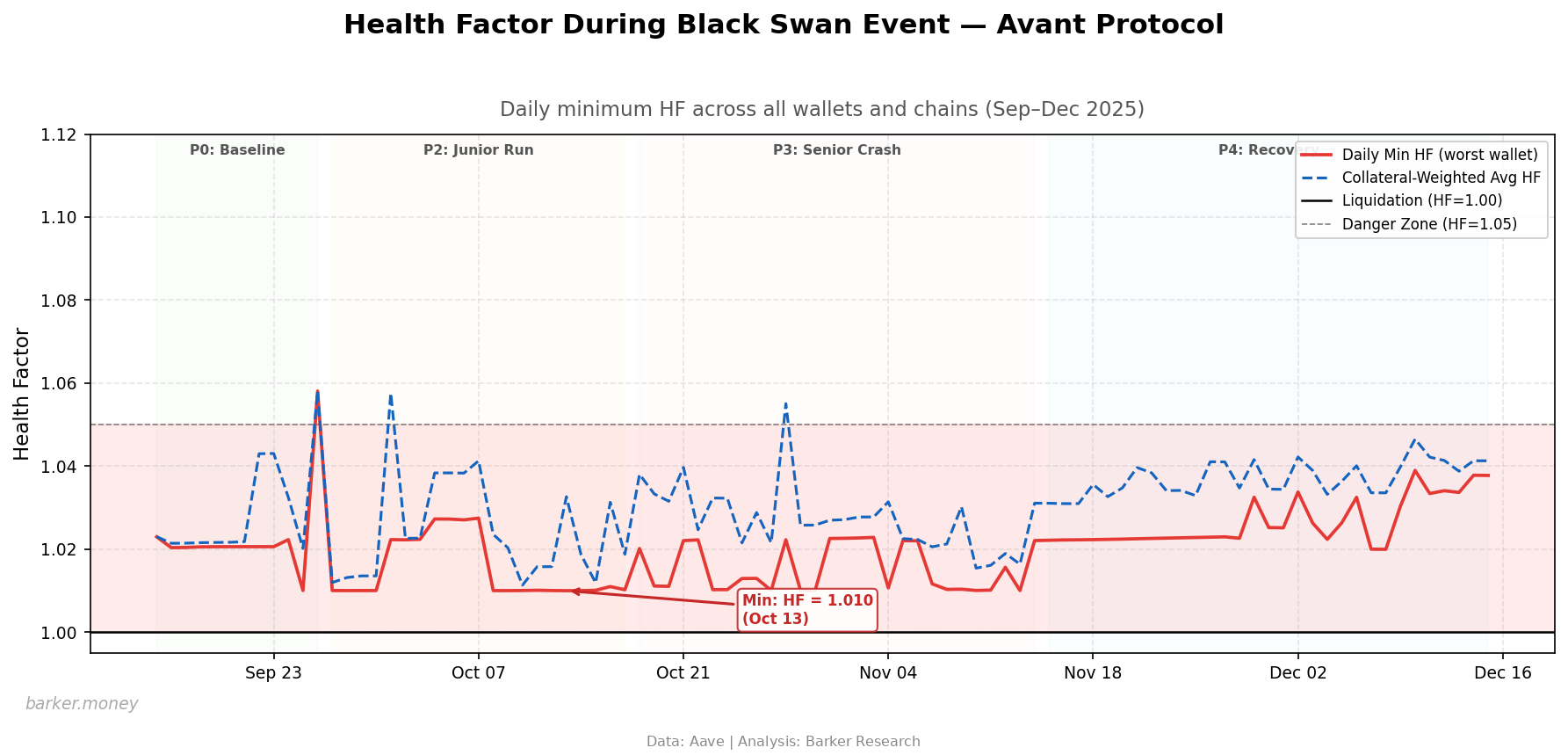

At 10x leverage with Health Factor persistently hugging 1.01–1.05, the strategy faces not only the "slow bleed" risk of being unable to unwind positions when spreads invert and liquidity dries up, but also a Sword of Damocles — cascading liquidation triggered by underlying stablecoin depegging.

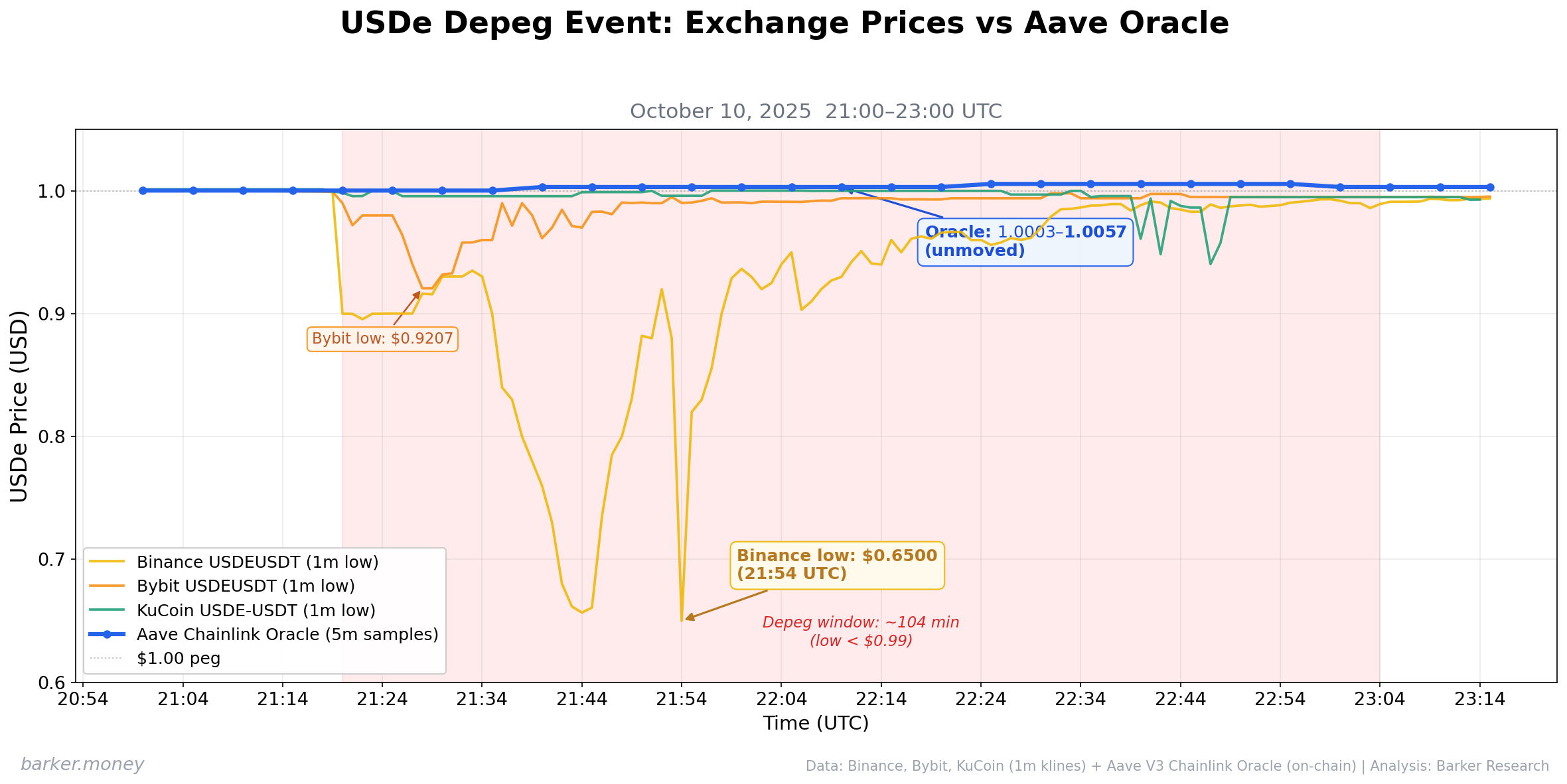

This is not a theoretical hypothetical. On October 10, 2025, USDe flash-crashed to $0.6500 on Binance's USDEUSDT pair (a 35% deviation from peg), while Bybit simultaneously dropped to $0.9207. Avant faced a genuine existential stress test. Since it survived, we must dissect how it pulled through:

The "oracle armor" that saved the protocol: Aave uses a Chainlink composite oracle that aggregates multiple data sources to filter out extreme single-exchange price spikes. We performed a minute-by-minute historical reconstruction of Aave's on-chain oracle during the event, sampling every 5 minutes. At the exact moment Binance was quoting $0.65, Chainlink's USDe price feed held rock-steady at $1.0003–$1.0057 — not only unfazed by the crash, but actually ticking slightly upward. Avant, thanks to this multi-source aggregation mechanism that filtered out extreme quotes, was fortunate to escape liquidation.

Yellow line: Binance 1-minute low price. Orange line: Bybit 1-minute low price. Green line: KuCoin 1-minute low price. Blue line: Aave Chainlink Oracle on-chain quote (5-minute samples). Using $0.99 as the depeg threshold, Binance remained in depeg for ~104 minutes (21:20–23:04 UTC). Binance bottomed at $0.6500, Bybit at $0.9207, KuCoin at $0.9404, while the Oracle held steady at $1.0003–$1.0057 throughout.

The Sword of Damocles (Extremely fragile safety margin): Despite avoiding liquidation, with HF reaching a low of 1.010, Chainlink's smoothed price needed to drop less than 1% more to trigger full-scale liquidation. This means that in a future depeg event, if selling pressure persists longer — forcing the oracle to lower its quote even slightly (say to $0.985) — cascading liquidation would be inevitable in this 10x leverage machine.

Red line shows daily minimum HF. October 13 hit 1.010, just 1% from liquidation. Over the entire 92-day observation period, 91 days saw HF below 1.05.

Avant did survive the dual shocks of October–November 2025 without triggering any liquidation. But this was primarily thanks to Aave oracle protection and the team's operational capability — not the tranche buffer mechanism.

Stress Test Replay: Where Did the Buffer Go During the Crisis?

Back to the core question: If a risk event occurs, can senior tranche users count on the buffer?

Given the current strategy structure, the answer is unequivocal: No.

Because strategy exposure is singular and highly concentrated, losses in the Ethena carry trade mean the senior tranche, junior tranche, and Reserve Fund would all be triggered simultaneously. All three architectural layers face the same risk source — there is no genuine underlying isolation.

Furthermore, the reserve fund as the first line of defense (just 1.4%, ~$1.27M) is woefully inadequate at critical moments. On-chain data shows that over 14 months of operation, despite the protocol generating an estimated $1M+ in performance fee revenue, the reserve pool only grew from $1M to $1.27M, primarily from its own yield strategy. Its capital injection pace has fallen far short of matching the protocol's massive scale growth.

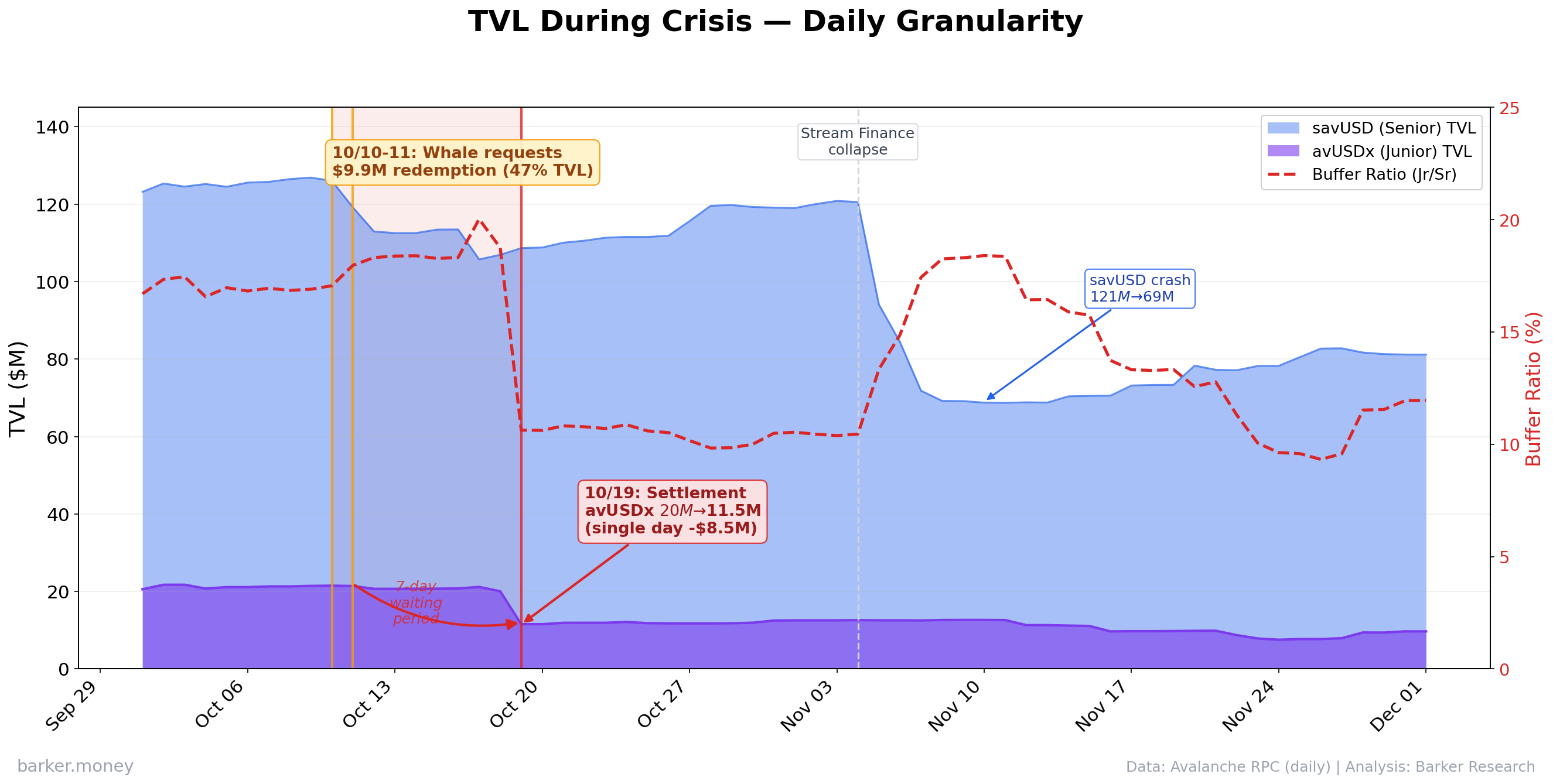

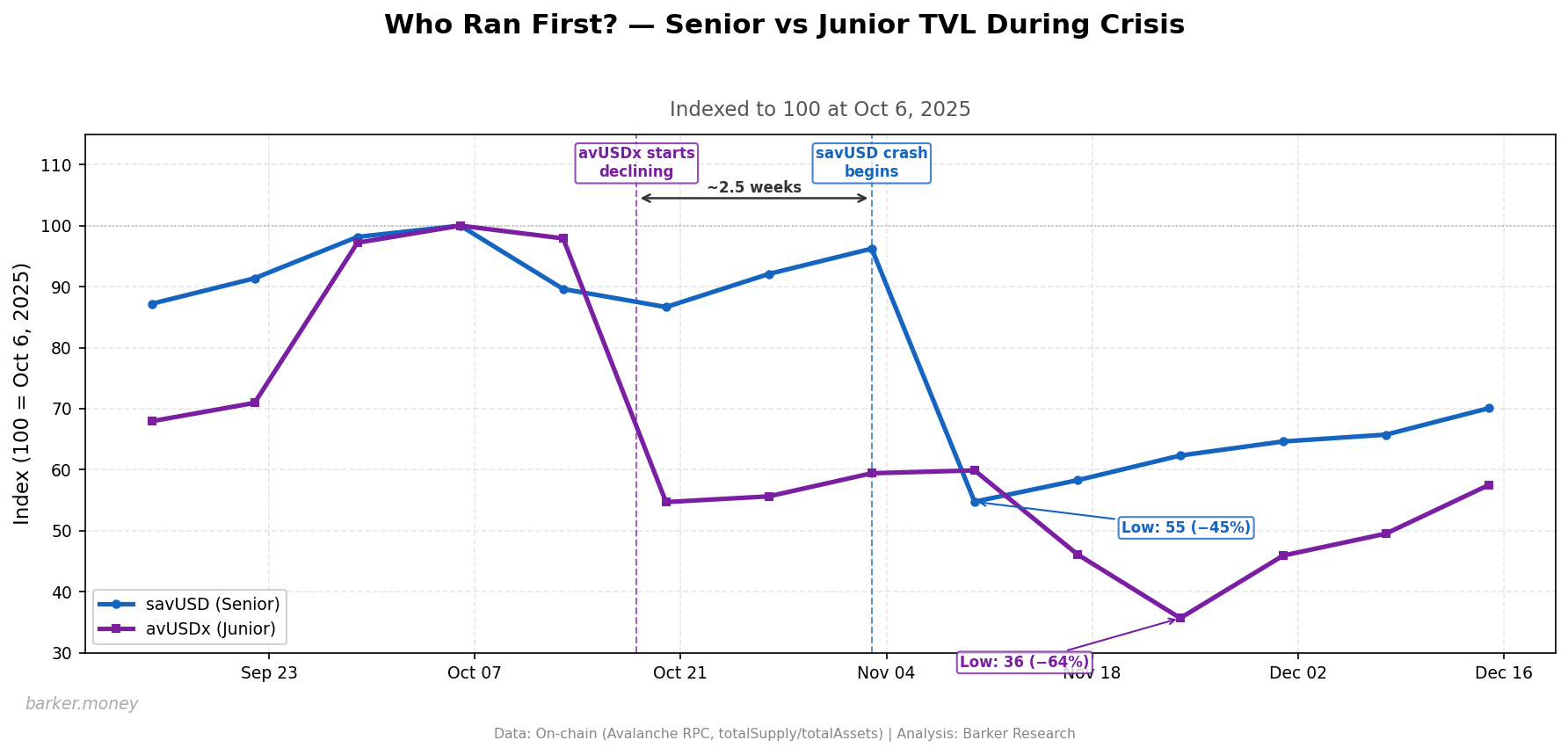

The October–November 2025 mass redemptions provide an excellent stress test sample. Through on-chain redemption transaction records, we fully reconstructed this junior tranche "front-running exodus":

Risk Instinct and Whale Front-Running (October 10–11)

When USDe came under price pressure on exchanges on October 10, with Aave Health Factors plunging to 1.010, junior capital reacted within hours. On-chain records show that nearly all selling pressure came from a single whale address (0x24de...). The whale initiated a first wave of $1.4M in redemptions on the 10th; then on the evening of the 11th, after USDe flash-crashed to $0.65, submitted 16 requests hitting the per-transaction maximum in just 13 minutes, totaling ~$8.7M.

Across just these two days of crisis, this single address submitted ~$9.9M in redemption requests — 47% of total junior tranche TVL ($21M) at the time. This was not blind retail panic, but the absolute rationality of large capital facing risk.

The Mechanism's Blind Spot: A Deadly "False Sense of Security"

avUSDx's mechanism includes a 7-day redemption waiting period. This design, intended to buffer liquidity shocks, instead created a counterintuitive trap during the crisis.

As shown in the table below, because redemption requests must wait 7 days before tokens are actually burned (removed from circulation), the nominal buffer ratio didn't fall when the whale was frantically requesting redemptions on Oct 10–11 — it actually rose slightly (from 16.8% to 18.0%).

| Date | Event | avUSDx/savUSD Nominal Buffer Ratio |

|---|---|---|

| Oct 06 | Pre-crisis baseline | 16.8% |

| Oct 10 | Alert: HF plunges, whale initiates $1.4M redemption | 16.8% (funds queued, not yet removed) |

| Oct 11 | Eruption: USDe flash crash, $8.7M in redemptions flood in within 13 min | 18.0% (same — creating visual illusion) |

| Oct 17–18 | Collapse: 7-day period expires, ~$10M settled en masse | 10.6% (halved in one day) |

| Nov 26 | Crisis aftermath bottoms out | 9.3% |

This delayed accounting created a dangerous false sense of security for senior tranche (savUSD) holders — the dashboard showed the buffer still intact, but in reality, nearly half the buffer capital had already been "locked for withdrawal." The protocol had entered a de facto "7-day countdown." Only when requests settled on October 17 did the buffer ratio suddenly collapse.

Blue area = savUSD TVL, purple area = avUSDx TVL, red dashed line (right axis) = avUSDx/savUSD buffer ratio. The buffer plunge on Oct 19 was the delayed settlement of the whale's front-running redemptions from 7 days prior.

This exposes a core pain point in current DeFi tranche protocols: the procyclicality of nominal buffers.

Genuine risk isolation requires junior capital to have long-term lock-up mechanisms or extremely high exit barriers. While Avant does impose a 7-day redemption waiting period, in the face of a real crisis, this short "cooling-off period" not only failed to lock in capital, but actually accelerated crisis transmission. Junior capital — by its very nature pursuing high volatility and high returns — is inevitably the most sensitive. Submitting requests early to front-run senior holders to the exit is their only rational choice.

The result: In calm markets, the buffer looks thick; at the protocol's darkest hour, the buffer gets rapidly drained. This is not an operational failure by the team, but an inevitable game-theoretic outcome of this tranche architecture.

IV. Our View

Avant is a product with noteworthy operational capability, but tranche protection should not be relied upon as a risk isolation mechanism.

What deserves recognition:

Avant has publicly disclosed 30 strategy wallet addresses and Reserve Fund balances, offering a relatively high level of transparency among comparable products. Under the extreme DeFi stress of October/November 2025, with HF reaching a low of 1.010, the team was fortunate not to trigger on-chain liquidation. savUSD has delivered 16% cumulative appreciation — the strategy execution capability deserves recognition.

What requires clear-eyed understanding:

Avant's underlying strategy is heavily concentrated in leveraged Ethena carry trade. As Ethena spreads have declined, the team has begun introducing new varieties like Syrup, bringing Ethena's share down from 90%+ to ~55%. But strategy types remain homogeneous lending rate arbitrage, still a considerable distance from the officially promoted "multi-strategy framework." More importantly, as spreads compress, this strategy's APY has inevitably declined from the early 20%+ to the current ~8%.

The tranche structure changes how yield is distributed — the junior tranche receives more yield and assumes nominal first-loss obligations — but it does not change the underlying homogeneity of risk.

Who is it for:

For users who understand and accept the risks of Ethena carry trade, savUSD/avUSDx offer a convenient entry point without needing to manage leveraged positions yourself. But the prerequisite is a thorough understanding that:

- You are effectively participating in ~10x leveraged Ethena carry trade, with the core risk being sUSDe/USDe depegging

- The tranche structure primarily affects yield distribution, not genuine risk isolation

- Under extreme market conditions, no layer can guarantee principal safety

Overall, Avant provides an extremely convenient gateway for ordinary users to access institutional-grade leveraged arbitrage returns, and its team's asset management and execution capabilities have withstood their initial test. But as sophisticated investors, we need to see through the marketing veneer of "tranching" and face the highly leveraged reality underneath —

In DeFi, risk never disappears — it is only redistributed and its exposure deferred.

Barker.Money — a one-stop stablecoin yield map helping individual users discover exchange and on-chain stablecoin opportunities that balance safety with relatively high returns. This article is the second installment of our "DeFi Yield Product Deep Dive" series. In the previous piece, we analyzed Unitas's yield amplification and reserve structure; this piece focuses on another common layered yield model — evaluating the risk isolation effectiveness of senior/junior tranche architectures. We have completed in-depth analysis of more yield-bearing stablecoins and DeFi pools, with subsequent publications to follow.

We also welcome community members to contribute independent analyses, working together to push this industry toward higher transparency standards.

Find yield. Find Barker.

Appendix

A. Methodology and Data Coverage

Classification note: The "Ethena carry" category in this report includes all Ethena ecosystem collateral — sUSDe, USDe, and Pendle PT-sUSDe / PT-USDe / PT-eUSDe fixed-income derivatives. PT assets account for ~18% of the Ethena carry classification, but their underlying risk exposure equally points to Ethena and would be impacted in the same direction during a USDe depeg event, hence the unified classification.

Data sources:

- Senior tranche: 23 strategy wallets, 6 EVM chains + Solana (Kamino) + Stacks (Zest)

- Junior tranche: 7 avUSDx strategy wallets (Pharaoh V3 / TraderJoe LB / Etherex / Morpho / Euler)

- Aave V3 HF and leverage: AAVE v3

- TVL: Avalanche RPC

- Rewarder injections: Complete record of 440 on-chain events

- Spread data: Aave V3 + DeFiLlama

B. Strategy Concentration History

| Period | Ethena Carry Share | Coverage |

|---|---|---|

| 2025-10 | 55–70% | 73–83% |

| 2025-11 | 83–94% | 83–90% |

| 2025-12 | 77–97% | 77–97% |

| 2026-01 | 80–94% | 84–97% |

| 2026-02 | 66–73% | 85–91% |

| 2026-03 | 52–66% | 84–87% |

| 2026-04 | 55% | 90% |

C. Leverage by Strategy

D. savUSD Historical Yield

Exchange Rate Quarterly Snapshots:

| Date | savUSD TVL | Exchange Rate | Cumulative Appreciation | Quarterly Change |

|---|---|---|---|---|

| 2025-01 (early stage) | $53.6M | 1.040941 | +4.1% | — |

| 2025-04 | $92.3M | 1.061066 | +6.1% | +1.93% |

| 2025-07 (peak TVL) | $119.3M | 1.095660 | +9.6% | +3.26% |

| 2025-10 | $91.5M | 1.128302 | +12.8% | +2.98% |

| 2026-01 | $84.8M | 1.147581 | +14.8% | +1.71% |

| 2026-04 (current) | $89.6M | 1.159142 | +15.9% | +1.01% |

The trend is clear: quarterly appreciation has declined steadily from a peak of +3.26% (Q2 2025) to +1.01% (Q1 2026), reflecting underlying spread compression.

Rolling Window Realized Annualized APY (Exchange Rate Method):

| Window | Realized Annualized APY |

|---|---|

| Full period (14 months) | ~13.5% |

| Trailing 6 months | ~12.4% |

| Trailing 3 months | ~9.7% |

| Trailing 2 months | ~8.0% |

| Trailing 5 weeks | ~7.7% |

E. October/November 2025 Black Swan Event Timeline

| Date | Event | Daily Min HF | avUSDx/savUSD Buffer Ratio |

|---|---|---|---|

| Oct 06 | Pre-crisis baseline | 1.027 | 16.8% |

| Oct 08 | Plasma HF first hits floor | 1.010 | 16.8% |

| Oct 10 | Ethereum HF plunges, whale's first $1.4M redemption wave | 1.010 | 16.8% |

| Oct 11 | USDe flash crash to $0.6567 on Binance, $8.7M redeemed in 13 min | 1.010 | 18.0% |

| Oct 16 | REWARDER emergency injection (daily amount +2.4x) | 1.011 | 18.3% |

| Oct 17 | 7-day waiting period expires, settlement begins | 1.010 | 20.0% |

| Oct 18 | Mass settlement in progress | 1.020 | 18.8% |

| Oct 19 | Buffer ratio halved in a single day | 1.011 | 10.6% |

| Oct 28 | Buffer continues probing lows | 1.022 | 9.8% |

| Nov 04 | Stream Finance bankruptcy event | 1.011 | 10.5% |

| Nov 08–11 | HF hits floor again, sustained 4 days | 1.010 | 18.4% |

| Nov 10 | savUSD collapses ($121M → $69M, −43%) | 1.010 | 18.4% |

| Nov 26 | Buffer lowest point | 1.023 | 9.3% |

| Dec 15 | Observation period ends, TVL stabilizes | 1.038 | 13.8% |

Data Sources

Avant Protocol Official Disclosures (30 strategy wallet addresses, Reserve Fund balances), Aave V3 On-chain Data (HF, leverage, oracle quotes), Avalanche RPC (TVL, REWARDER injection events), DeFiLlama, Barker DB

All data in this report comes from public disclosures and on-chain data. This does not constitute investment advice.